Can the “IRA One-Rollover-Per-Year-Rule” affect the division of property?

The IRS new rule “IRA One-Rollover-Per-Year-Rule” may affect the division of property in a divorce. We use to think that dividing an IRA was simple, there was no need for a QDRO, just the language in the Divorce Decree. Well, effective as early as January 1, 2015 an individual will only be allowed to make one rollover from an IRA to another (or the same) IRA in any 12-month period. You will, however be allowed to continue to make trustee-to-trustee transfers between IRAs. You can also make as many rollovers from traditional IRAs to Roth IRAs as you want.

The Tax Court recently held that you CAN NOT make a non-taxable rollover from one IRA to another if you have already made a rollover from any of your IRAs in the preceding 1-year period (Bobrow v Commissioner, T.C. Memo 2014-21). Following this decision means:

- You must include in gross income nay previously untaxed amounts distributed from an IRA if you made an IRA-to-IRA rollover in the preceding 12 months, and

- You may be subject to the 10% early withdrawal tax on the amount you include in gross income.

Additionally, if you pay these amounts into another (or the same) IRA, they may be:

- Excess contributions, and

- Taxed at 6% per year as long as they remain in the IRA.

The IRS indicates that this change will not affect an individual’s ability to transfer funds from one IRA trustee directly to another, because this type of transfer isn’t a rollover. Per the IRS the one-per year limit does not apply to:

rollovers from traditional IRAs to Roth IRAs (conversions)

- trustee-to-trustee transfers to another IRA

- IRA-to-plan rollovers

- plan-to-IRA rollovers

- plan-to-plan rollovers

If you are in the process of settlement negotiations, and were expecting to have a final trial or mediation after January 1, 2015, you will want to take this change into consideration. If your trial date or mediation is already scheduled contact the trustee of the IRAs and determine 1) what type of IRAs you are dealing with, 2) if a party can open an IRA and have funds transferred into the new account without being considered a rollover, 2) if your client is eligible to open the IRA in their name or in the name of their spouse, 3) how long it will take to set up the new account, 4) if they have a standardized form indicating that the action to be classified a transfer and not a roll-over, 5) what is the verbiage that needs to be in the divorce decree for this action to be classified a transfer and not a roll-over.

If your client is the receiving party and they are not allowed to set up an IRA through that particular trustee they will need to contact another institution and find out exactly what they will need to do to accomplish the division to be classified as a transfer and not a roll-over. If it is deemed that no matter how the division is handled your client will be affected by the “IRA One-Rollover-Per-Year Rule” you will need to adjust the value based on the potential tax risk.

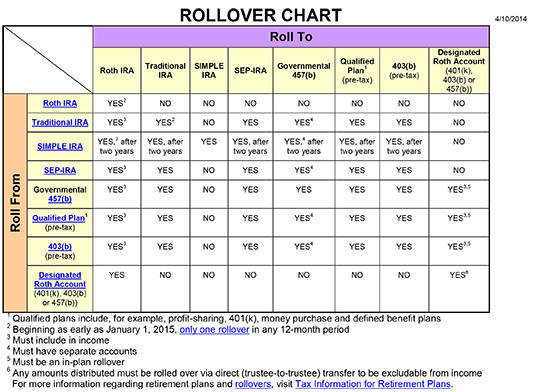

Below is the current IRS ROLLOVER CHART: